{kind=link}

House Price Prediction

This is the first practice for machine learning and for Kaggle competition: House Prices: Advanced Regression Techniques. Using Ridge, Lasso, LGBM, XGB, Stacking CV Regressor, and etc, to reach Score(mean absolute error): 11977.59807; 13th place out of 19,465 teams (0.06%) For more information, please see my project directly or visit my Github Repository.

![]()

version 1: Simple Prediction(with ridge regression, random forest, bagging, XGBoost) View PDF

version 2: Score(root mean squared logarithmic error): 0.10643; Rank: top 2%. score: 0.10643;

version3: Score(mean absolute error): 11977.59807; Rank: 13 out of 19,465 teams(0.06%)

House Price Prediction — version 2

Charles Zhang Jan 19 2020

Introduction

This is my second version House Price Prediction Model for the Kaggle Competition. In this version, I improve methods for processing missing value more accurately, use Ridge, Lasso, LGBM, XGB, and Stacking CV Regressor to build machie learning models, and add blended models. Since some contents are repeated, I will just breifly describe the dataset at the beginning.

# This Python 3 environment comes with many helpful analytics libraries installed

# It is defined by the kaggle/python docker image: https://github.com/kaggle/docker-python

# For example, here's several helpful packages to load in

import numpy as np # linear algebra

import pandas as pd # data processing, CSV file I/O (e.g. pd.read_csv)

# Input data files are available in the "../input/" directory.

# For example, running this (by clicking run or pressing Shift+Enter) will list the files in the input directory

import matplotlib.gridspec as gridspec

from datetime import datetime

from scipy.stats import skew # for some statistics

from scipy.special import boxcox1p

from scipy.stats import boxcox_normmax

from sklearn.linear_model import ElasticNetCV, LassoCV, RidgeCV

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.svm import SVR

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import RobustScaler

from sklearn.model_selection import KFold, cross_val_score

from sklearn.metrics import mean_squared_error

from mlxtend.regressor import StackingCVRegressor

from xgboost import XGBRegressor

from lightgbm import LGBMRegressor

import matplotlib.pyplot as plt

import scipy.stats as stats

import sklearn.linear_model as linear_model

import matplotlib.style as style

import seaborn as sns

from sklearn.manifold import TSNE

from sklearn.cluster import KMeans

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

import warnings

warnings.filterwarnings('ignore')

# Any results you write to the current directory are saved as output.

A Glimpse of the datasets.

train = pd.read_csv("../input/house-prices-advanced-regression-techniques/train.csv")

test = pd.read_csv("../input/house-prices-advanced-regression-techniques/test.csv")

# gives us statistical info about the numerical variables.

train.describe().T

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| Id | 1460.0 | 730.500000 | 421.610009 | 1.0 | 365.75 | 730.5 | 1095.25 | 1460.0 |

| MSSubClass | 1460.0 | 56.897260 | 42.300571 | 20.0 | 20.00 | 50.0 | 70.00 | 190.0 |

| LotFrontage | 1201.0 | 70.049958 | 24.284752 | 21.0 | 59.00 | 69.0 | 80.00 | 313.0 |

| LotArea | 1460.0 | 10516.828082 | 9981.264932 | 1300.0 | 7553.50 | 9478.5 | 11601.50 | 215245.0 |

| OverallQual | 1460.0 | 6.099315 | 1.382997 | 1.0 | 5.00 | 6.0 | 7.00 | 10.0 |

| OverallCond | 1460.0 | 5.575342 | 1.112799 | 1.0 | 5.00 | 5.0 | 6.00 | 9.0 |

| YearBuilt | 1460.0 | 1971.267808 | 30.202904 | 1872.0 | 1954.00 | 1973.0 | 2000.00 | 2010.0 |

| YearRemodAdd | 1460.0 | 1984.865753 | 20.645407 | 1950.0 | 1967.00 | 1994.0 | 2004.00 | 2010.0 |

| MasVnrArea | 1452.0 | 103.685262 | 181.066207 | 0.0 | 0.00 | 0.0 | 166.00 | 1600.0 |

| BsmtFinSF1 | 1460.0 | 443.639726 | 456.098091 | 0.0 | 0.00 | 383.5 | 712.25 | 5644.0 |

| BsmtFinSF2 | 1460.0 | 46.549315 | 161.319273 | 0.0 | 0.00 | 0.0 | 0.00 | 1474.0 |

| BsmtUnfSF | 1460.0 | 567.240411 | 441.866955 | 0.0 | 223.00 | 477.5 | 808.00 | 2336.0 |

| TotalBsmtSF | 1460.0 | 1057.429452 | 438.705324 | 0.0 | 795.75 | 991.5 | 1298.25 | 6110.0 |

| 1stFlrSF | 1460.0 | 1162.626712 | 386.587738 | 334.0 | 882.00 | 1087.0 | 1391.25 | 4692.0 |

| 2ndFlrSF | 1460.0 | 346.992466 | 436.528436 | 0.0 | 0.00 | 0.0 | 728.00 | 2065.0 |

| LowQualFinSF | 1460.0 | 5.844521 | 48.623081 | 0.0 | 0.00 | 0.0 | 0.00 | 572.0 |

| GrLivArea | 1460.0 | 1515.463699 | 525.480383 | 334.0 | 1129.50 | 1464.0 | 1776.75 | 5642.0 |

| BsmtFullBath | 1460.0 | 0.425342 | 0.518911 | 0.0 | 0.00 | 0.0 | 1.00 | 3.0 |

| BsmtHalfBath | 1460.0 | 0.057534 | 0.238753 | 0.0 | 0.00 | 0.0 | 0.00 | 2.0 |

| FullBath | 1460.0 | 1.565068 | 0.550916 | 0.0 | 1.00 | 2.0 | 2.00 | 3.0 |

| HalfBath | 1460.0 | 0.382877 | 0.502885 | 0.0 | 0.00 | 0.0 | 1.00 | 2.0 |

| BedroomAbvGr | 1460.0 | 2.866438 | 0.815778 | 0.0 | 2.00 | 3.0 | 3.00 | 8.0 |

| KitchenAbvGr | 1460.0 | 1.046575 | 0.220338 | 0.0 | 1.00 | 1.0 | 1.00 | 3.0 |

| TotRmsAbvGrd | 1460.0 | 6.517808 | 1.625393 | 2.0 | 5.00 | 6.0 | 7.00 | 14.0 |

| Fireplaces | 1460.0 | 0.613014 | 0.644666 | 0.0 | 0.00 | 1.0 | 1.00 | 3.0 |

| GarageYrBlt | 1379.0 | 1978.506164 | 24.689725 | 1900.0 | 1961.00 | 1980.0 | 2002.00 | 2010.0 |

| GarageCars | 1460.0 | 1.767123 | 0.747315 | 0.0 | 1.00 | 2.0 | 2.00 | 4.0 |

| GarageArea | 1460.0 | 472.980137 | 213.804841 | 0.0 | 334.50 | 480.0 | 576.00 | 1418.0 |

| WoodDeckSF | 1460.0 | 94.244521 | 125.338794 | 0.0 | 0.00 | 0.0 | 168.00 | 857.0 |

| OpenPorchSF | 1460.0 | 46.660274 | 66.256028 | 0.0 | 0.00 | 25.0 | 68.00 | 547.0 |

| EnclosedPorch | 1460.0 | 21.954110 | 61.119149 | 0.0 | 0.00 | 0.0 | 0.00 | 552.0 |

| 3SsnPorch | 1460.0 | 3.409589 | 29.317331 | 0.0 | 0.00 | 0.0 | 0.00 | 508.0 |

| ScreenPorch | 1460.0 | 15.060959 | 55.757415 | 0.0 | 0.00 | 0.0 | 0.00 | 480.0 |

| PoolArea | 1460.0 | 2.758904 | 40.177307 | 0.0 | 0.00 | 0.0 | 0.00 | 738.0 |

| MiscVal | 1460.0 | 43.489041 | 496.123024 | 0.0 | 0.00 | 0.0 | 0.00 | 15500.0 |

| MoSold | 1460.0 | 6.321918 | 2.703626 | 1.0 | 5.00 | 6.0 | 8.00 | 12.0 |

| YrSold | 1460.0 | 2007.815753 | 1.328095 | 2006.0 | 2007.00 | 2008.0 | 2009.00 | 2010.0 |

| SalePrice | 1460.0 | 180921.195890 | 79442.502883 | 34900.0 | 129975.00 | 163000.0 | 214000.00 | 755000.0 |

Checking for Missing Values

Missing Train values

def missing_percentage(df):

"""This function takes a DataFrame(df) as input and returns two columns, total missing values and total missing values percentage"""

## the two following line may seem complicated but its actually very simple.

total = df.isnull().sum().sort_values(ascending = False)[df.isnull().sum().sort_values(ascending = False) != 0]

percent = round(df.isnull().sum().sort_values(ascending = False)/len(df)*100,2)[round(df.isnull().sum().sort_values(ascending = False)/len(df)*100,2) != 0]

return pd.concat([total, percent], axis=1, keys=['Total','Percent'])

missing_percentage(train)

| Total | Percent | |

|---|---|---|

| PoolQC | 1453 | 99.52 |

| MiscFeature | 1406 | 96.30 |

| Alley | 1369 | 93.77 |

| Fence | 1179 | 80.75 |

| FireplaceQu | 690 | 47.26 |

| LotFrontage | 259 | 17.74 |

| GarageCond | 81 | 5.55 |

| GarageType | 81 | 5.55 |

| GarageYrBlt | 81 | 5.55 |

| GarageFinish | 81 | 5.55 |

| GarageQual | 81 | 5.55 |

| BsmtExposure | 38 | 2.60 |

| BsmtFinType2 | 38 | 2.60 |

| BsmtFinType1 | 37 | 2.53 |

| BsmtCond | 37 | 2.53 |

| BsmtQual | 37 | 2.53 |

| MasVnrArea | 8 | 0.55 |

| MasVnrType | 8 | 0.55 |

| Electrical | 1 | 0.07 |

Missing Test values

missing_percentage(test)

| Total | Percent | |

|---|---|---|

| PoolQC | 1456 | 99.79 |

| MiscFeature | 1408 | 96.50 |

| Alley | 1352 | 92.67 |

| Fence | 1169 | 80.12 |

| FireplaceQu | 730 | 50.03 |

| LotFrontage | 227 | 15.56 |

| GarageCond | 78 | 5.35 |

| GarageQual | 78 | 5.35 |

| GarageYrBlt | 78 | 5.35 |

| GarageFinish | 78 | 5.35 |

| GarageType | 76 | 5.21 |

| BsmtCond | 45 | 3.08 |

| BsmtQual | 44 | 3.02 |

| BsmtExposure | 44 | 3.02 |

| BsmtFinType1 | 42 | 2.88 |

| BsmtFinType2 | 42 | 2.88 |

| MasVnrType | 16 | 1.10 |

| MasVnrArea | 15 | 1.03 |

| MSZoning | 4 | 0.27 |

| BsmtHalfBath | 2 | 0.14 |

| Utilities | 2 | 0.14 |

| Functional | 2 | 0.14 |

| BsmtFullBath | 2 | 0.14 |

| BsmtFinSF2 | 1 | 0.07 |

| BsmtFinSF1 | 1 | 0.07 |

| Exterior2nd | 1 | 0.07 |

| BsmtUnfSF | 1 | 0.07 |

| TotalBsmtSF | 1 | 0.07 |

| SaleType | 1 | 0.07 |

| Exterior1st | 1 | 0.07 |

| KitchenQual | 1 | 0.07 |

| GarageArea | 1 | 0.07 |

| GarageCars | 1 | 0.07 |

Observation

- There are multiple types of features.

- Some features have missing values.

- Most of the features are object( includes string values in the variable).

Similarly, I will normalize the distrbution of the SalePrice by log next.

def plotting_3_chart(df, feature):

## Importing seaborn, matplotlab and scipy modules.

import seaborn as sns

import matplotlib.gridspec as gridspec

import matplotlib.pyplot as plt

from scipy import stats

import matplotlib.style as style

style.use('fivethirtyeight')

## Creating a customized chart. and giving in figsize and everything.

fig = plt.figure(constrained_layout=True, figsize=(15,10))

## creating a grid of 3 cols and 3 rows.

grid = gridspec.GridSpec(ncols=3, nrows=3, figure=fig)

#gs = fig3.add_gridspec(3, 3)

## Customizing the histogram grid.

ax1 = fig.add_subplot(grid[0, :2])

## Set the title.

ax1.set_title('Histogram')

## plot the histogram.

sns.distplot(df.loc[:,feature], norm_hist=True, ax = ax1)

# customizing the QQ_plot.

ax2 = fig.add_subplot(grid[1, :2])

## Set the title.

ax2.set_title('QQ_plot')

## Plotting the QQ_Plot.

stats.probplot(df.loc[:,feature], plot = ax2)

## Customizing the Box Plot.

ax3 = fig.add_subplot(grid[:, 2])

## Set title.

ax3.set_title('Box Plot')

## Plotting the box plot.

sns.boxplot(df.loc[:,feature], orient='v', ax = ax3 );

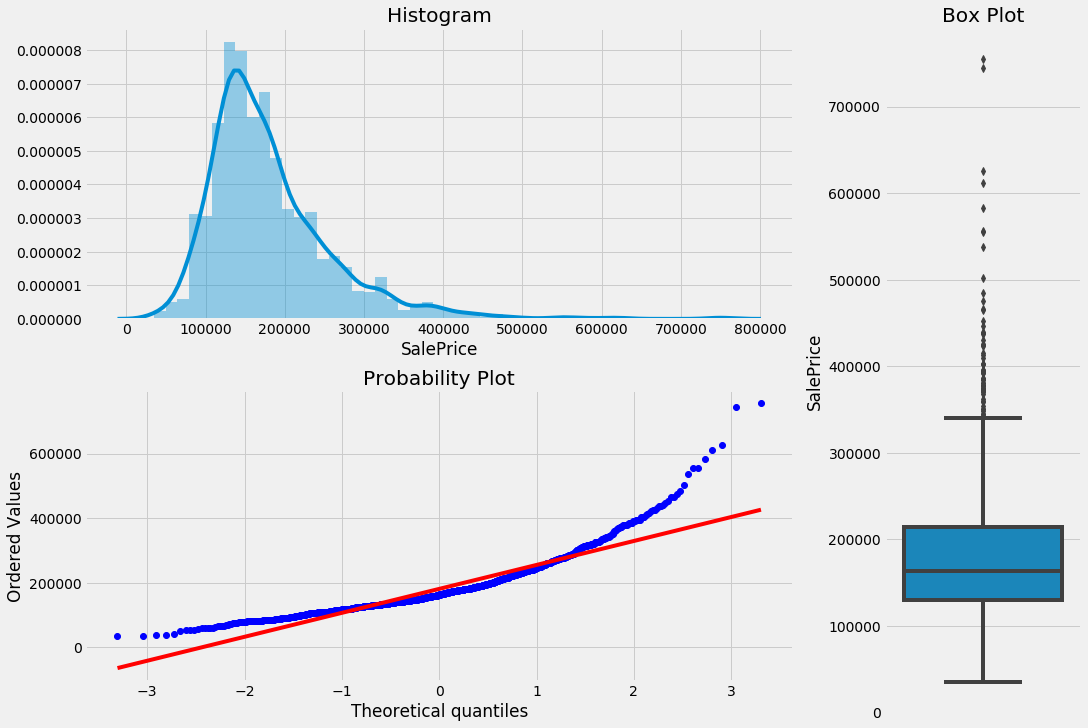

plotting_3_chart(train, 'SalePrice')

These three charts above can tell us a lot about our target variable.

- Our target variable, SalePrice is not normally distributed.

- Our target variable is right-skewed.

- There are multiple outliers in the variable.

#skewness and kurtosis

print("Skewness: " + str(train['SalePrice'].skew()))

print("Kurtosis: " + str(train['SalePrice'].kurt()))

Skewness: 1.8828757597682129

Kurtosis: 6.536281860064529

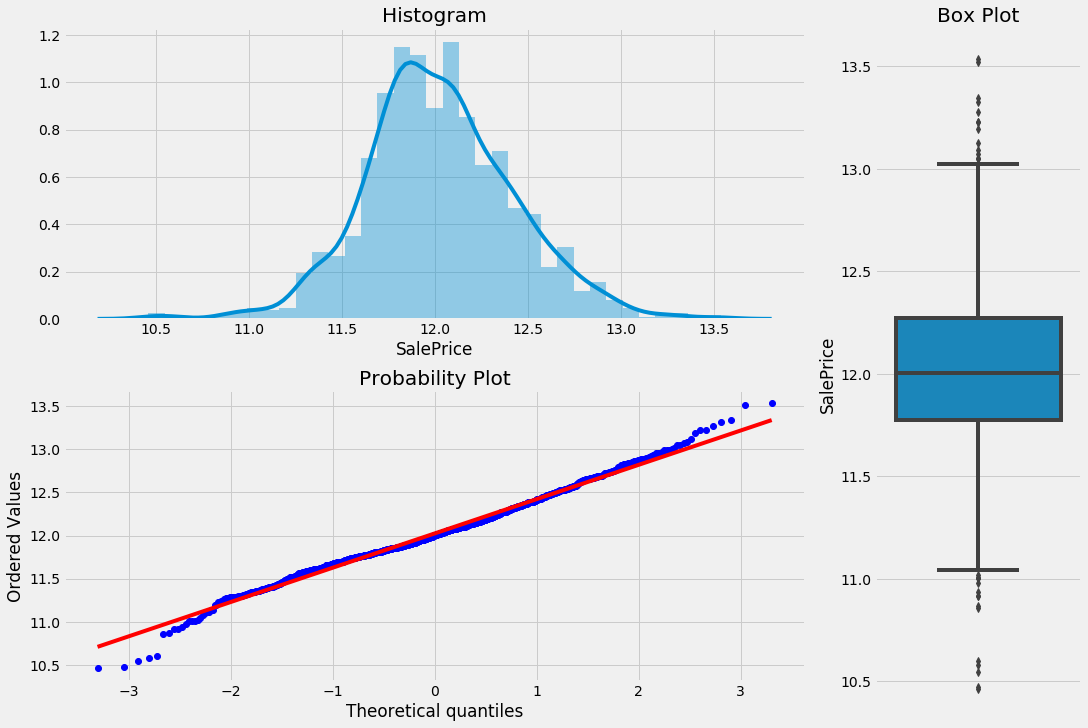

## trainsforming target variable using numpy.log1p,

train["SalePrice"] = np.log1p(train["SalePrice"])

## Plotting the newly transformed response variable

plotting_3_chart(train, 'SalePrice')

As you can see the log transformation removes the normality of errors. This solves some of the other assumptions that we talked about above like Homoscedasticity. Let’s make a comparison of the pre-transformed and post-transformed state of residual plots.

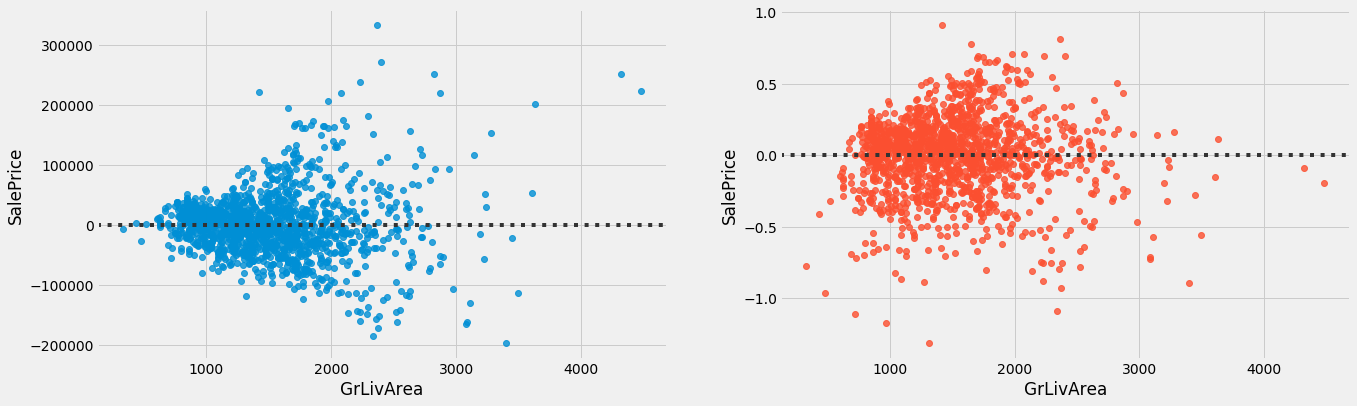

## Customizing grid for two plots.

fig, (ax1, ax2) = plt.subplots(figsize = (20,6), ncols=2, sharey = False, sharex=False)

## doing the first scatter plot.

sns.residplot(x = previous_train.GrLivArea, y = previous_train.SalePrice, ax = ax1)

## doing the scatter plot for GrLivArea and SalePrice.

sns.residplot(x = train.GrLivArea, y = train.SalePrice, ax = ax2);

Here, we can see that the pre-transformed chart on the left has heteroscedasticity, and the post-transformed chart on the right has almost an equal amount of variance across the zero lines.

## Plot fig sizing.

style.use('ggplot')

sns.set_style('whitegrid')

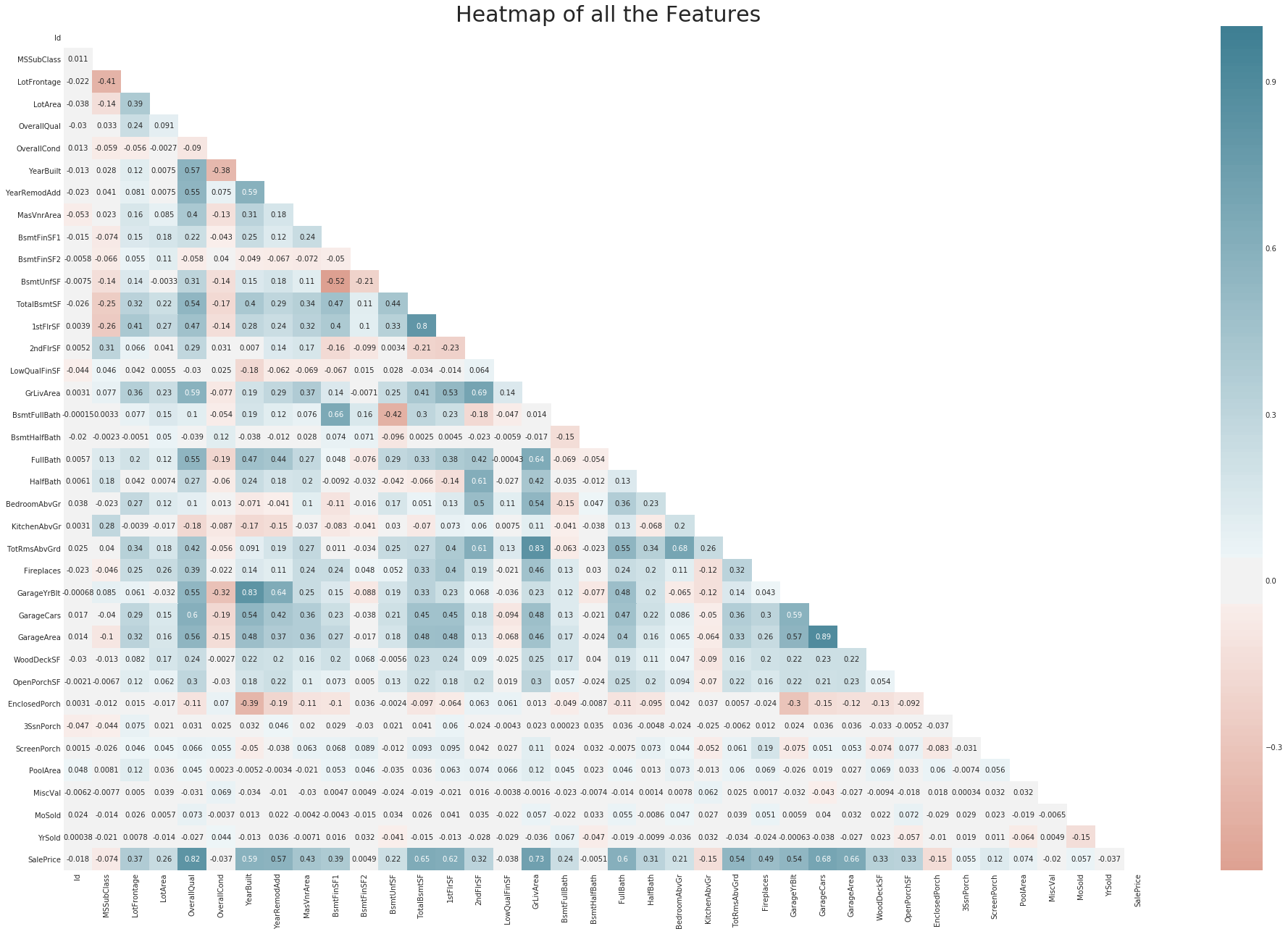

plt.subplots(figsize = (30,20))

## Plotting heatmap.

# Generate a mask for the upper triangle (taken from seaborn example gallery)

mask = np.zeros_like(train.corr(), dtype=np.bool)

mask[np.triu_indices_from(mask)] = True

sns.heatmap(train.corr(), cmap=sns.diverging_palette(20, 220, n=200), mask = mask, annot=True, center = 0, );

## Give title.

plt.title("Heatmap of all the Features", fontsize = 30);

## Dropping the "Id" from train and test set.

# train.drop(columns=['Id'],axis=1, inplace=True)

train.drop(columns=['Id'],axis=1, inplace=True)

test.drop(columns=['Id'],axis=1, inplace=True)

## Saving the target values in "y_train".

y = train['SalePrice'].reset_index(drop=True)

# getting a copy of train

previous_train = train.copy()

## Combining train and test datasets together so that we can do all the work at once.

all_data = pd.concat((train, test)).reset_index(drop = True)

## Dropping the target variable.

all_data.drop(['SalePrice'], axis = 1, inplace = True)

Dealing with Missing Values

Missing data in train and test data(all_data)

Imputing Missing Values

## Some missing values are intentionally left blank, for example: In the Alley feature

## there are blank values meaning that there are no alley's in that specific house.

missing_val_col = ["Alley",

"PoolQC",

"MiscFeature",

"Fence",

"FireplaceQu",

"GarageType",

"GarageFinish",

"GarageQual",

"GarageCond",

'BsmtQual',

'BsmtCond',

'BsmtExposure',

'BsmtFinType1',

'BsmtFinType2',

'MasVnrType']

for i in missing_val_col:

all_data[i] = all_data[i].fillna('None')

## These features are continous variable, we used "0" to replace the null values.

missing_val_col2 = ['BsmtFinSF1',

'BsmtFinSF2',

'BsmtUnfSF',

'TotalBsmtSF',

'BsmtFullBath',

'BsmtHalfBath',

'GarageYrBlt',

'GarageArea',

'GarageCars',

'MasVnrArea']

for i in missing_val_col2:

all_data[i] = all_data[i].fillna(0)

## Replaced all missing values in LotFrontage by imputing the median value of each neighborhood.

all_data['LotFrontage'] = all_data.groupby('Neighborhood')['LotFrontage'].transform( lambda x: x.fillna(x.mean()))

## the "OverallCond" and "OverallQual" of the house.

# all_data['OverallCond'] = all_data['OverallCond'].astype(str)

# all_data['OverallQual'] = all_data['OverallQual'].astype(str)

## Zoning class are given in numerical; therefore converted to categorical variables.

all_data['MSSubClass'] = all_data['MSSubClass'].astype(str)

all_data['MSZoning'] = all_data.groupby('MSSubClass')['MSZoning'].transform(lambda x: x.fillna(x.mode()[0]))

## Important years and months that should be categorical variables not numerical.

# all_data['YearBuilt'] = all_data['YearBuilt'].astype(str)

# all_data['YearRemodAdd'] = all_data['YearRemodAdd'].astype(str)

# all_data['GarageYrBlt'] = all_data['GarageYrBlt'].astype(str)

all_data['YrSold'] = all_data['YrSold'].astype(str)

all_data['MoSold'] = all_data['MoSold'].astype(str)

all_data['Functional'] = all_data['Functional'].fillna('Typ')

all_data['Utilities'] = all_data['Utilities'].fillna('AllPub')

all_data['Exterior1st'] = all_data['Exterior1st'].fillna(all_data['Exterior1st'].mode()[0])

all_data['Exterior2nd'] = all_data['Exterior2nd'].fillna(all_data['Exterior2nd'].mode()[0])

all_data['KitchenQual'] = all_data['KitchenQual'].fillna("TA")

all_data['SaleType'] = all_data['SaleType'].fillna(all_data['SaleType'].mode()[0])

all_data['Electrical'] = all_data['Electrical'].fillna("SBrkr")

missing_percentage(all_data)

| Total | Percent |

|---|

So, there are no missing value left.

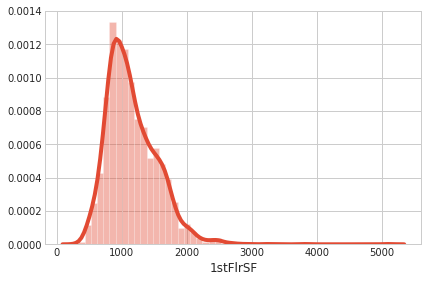

sns.distplot(all_data['1stFlrSF']);

numeric_feats = all_data.dtypes[all_data.dtypes != "object"].index

skewed_feats = all_data[numeric_feats].apply(lambda x: skew(x)).sort_values(ascending=False)

skewed_feats

MiscVal 21.939672

PoolArea 17.688664

LotArea 13.109495

LowQualFinSF 12.084539

3SsnPorch 11.372080

KitchenAbvGr 4.300550

BsmtFinSF2 4.144503

EnclosedPorch 4.002344

ScreenPorch 3.945101

BsmtHalfBath 3.929996

MasVnrArea 2.621719

OpenPorchSF 2.529358

WoodDeckSF 1.844792

1stFlrSF 1.257286

GrLivArea 1.068750

LotFrontage 1.058803

BsmtFinSF1 0.980645

BsmtUnfSF 0.919688

2ndFlrSF 0.861556

TotRmsAbvGrd 0.749232

Fireplaces 0.725278

HalfBath 0.696666

TotalBsmtSF 0.671751

BsmtFullBath 0.622415

OverallCond 0.569314

BedroomAbvGr 0.326568

GarageArea 0.216857

OverallQual 0.189591

FullBath 0.165514

GarageCars -0.219297

YearRemodAdd -0.450134

YearBuilt -0.599194

GarageYrBlt -3.904632

dtype: float64

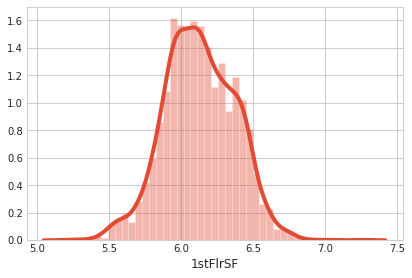

## Fixing Skewed features using boxcox transformation.

def fixing_skewness(df):

"""

This function takes in a dataframe and return fixed skewed dataframe

"""

## Import necessary modules

from scipy.stats import skew

from scipy.special import boxcox1p

from scipy.stats import boxcox_normmax

## Getting all the data that are not of "object" type.

numeric_feats = df.dtypes[df.dtypes != "object"].index

# Check the skew of all numerical features

skewed_feats = df[numeric_feats].apply(lambda x: skew(x)).sort_values(ascending=False)

high_skew = skewed_feats[abs(skewed_feats) > 0.5]

skewed_features = high_skew.index

for feat in skewed_features:

df[feat] = boxcox1p(df[feat], boxcox_normmax(df[feat] + 1))

fixing_skewness(all_data)

sns.distplot(all_data['1stFlrSF']);

all_data = all_data.drop(['Utilities', 'Street', 'PoolQC',], axis=1)

# feture engineering a new feature "TotalFS"

all_data['TotalSF'] = all_data['TotalBsmtSF'] + all_data['1stFlrSF'] + all_data['2ndFlrSF']

all_data['YrBltAndRemod']=all_data['YearBuilt']+all_data['YearRemodAdd']

all_data['Total_sqr_footage'] = (all_data['BsmtFinSF1'] + all_data['BsmtFinSF2'] +

all_data['1stFlrSF'] + all_data['2ndFlrSF'])

all_data['Total_Bathrooms'] = (all_data['FullBath'] + (0.5 * all_data['HalfBath']) +

all_data['BsmtFullBath'] + (0.5 * all_data['BsmtHalfBath']))

all_data['Total_porch_sf'] = (all_data['OpenPorchSF'] + all_data['3SsnPorch'] +

all_data['EnclosedPorch'] + all_data['ScreenPorch'] +

all_data['WoodDeckSF'])

all_data['haspool'] = all_data['PoolArea'].apply(lambda x: 1 if x > 0 else 0)

all_data['has2ndfloor'] = all_data['2ndFlrSF'].apply(lambda x: 1 if x > 0 else 0)

all_data['hasgarage'] = all_data['GarageArea'].apply(lambda x: 1 if x > 0 else 0)

all_data['hasbsmt'] = all_data['TotalBsmtSF'].apply(lambda x: 1 if x > 0 else 0)

all_data['hasfireplace'] = all_data['Fireplaces'].apply(lambda x: 1 if x > 0 else 0)

all_data.shape

(2917, 86)

Creating Dummy Variables.

## Creating dummy variable

final_features = pd.get_dummies(all_data).reset_index(drop=True)

final_features.shape

(2917, 333)

X = final_features.iloc[:len(y), :]

X_sub = final_features.iloc[len(y):, :]

outliers = [30, 88, 462, 631, 1322]

X = X.drop(X.index[outliers])

y = y.drop(y.index[outliers])

def overfit_reducer(df):

"""

This function takes in a dataframe and returns a list of features that are overfitted.

"""

overfit = []

for i in df.columns:

counts = df[i].value_counts()

zeros = counts.iloc[0]

if zeros / len(df) * 100 > 99.94:

overfit.append(i)

overfit = list(overfit)

return overfit

overfitted_features = overfit_reducer(X)

X = X.drop(overfitted_features, axis=1)

X_sub = X_sub.drop(overfitted_features, axis=1)

X.shape,y.shape, X_sub.shape

((1453, 332), (1453,), (1459, 332))

Fitting model(simple approach)

Train_test split

## Train test s

from sklearn.model_selection import train_test_split

## Train test split follows this distinguished code pattern and helps creating train and test set to build machine learning.

X_train, X_test, y_train, y_test = train_test_split(X, y,test_size = .33, random_state = 0)

X_train.shape, y_train.shape, X_test.shape, y_test.shape

((973, 332), (973,), (480, 332), (480,))

Regularization Models

What makes regression model more effective is its ability of regularizing. The term “regularizing” stands for models ability to structurally prevent overfitting by imposing a penalty on the coefficients.

There are three types of regularizations.

- Ridge

- Lasso

- Elastic Net

Ridge:

Ridge regression adds penalty equivalent to the square of the magnitude of the coefficients. This penalty is added to the least square loss function above and looks like this…

## Importing Ridge.

from sklearn.linear_model import Ridge

from sklearn.metrics import mean_absolute_error, mean_squared_error

## Assiging different sets of alpha values to explore which can be the best fit for the model.

alpha_ridge = [-3,-2,-1,1e-15, 1e-10, 1e-8,1e-5,1e-4, 1e-3,1e-2,0.5,1,1.5, 2,3,4, 5, 10, 20, 30, 40]

temp_rss = {}

temp_mse = {}

for i in alpha_ridge:

## Assigin each model.

ridge = Ridge(alpha= i, normalize=True)

## fit the model.

ridge.fit(X_train, y_train)

## Predicting the target value based on "Test_x"

y_pred = ridge.predict(X_test)

mse = mean_squared_error(y_test, y_pred)

rss = sum((y_pred-y_test)**2)

temp_mse[i] = mse

temp_rss[i] = rss

for key, value in sorted(temp_mse.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.01: 0.012058094362558029

0.001: 0.012361806597259932

0.5: 0.012398339976451882

0.0001: 0.01245484128284161

1e-05: 0.012608710731947215

1e-15: 0.0126876442980313

1e-08: 0.012689390127616456

1e-10: 0.012689491191917741

1: 0.013828461568989092

1.5: 0.015292912807173023

2: 0.016759826630923253

3: 0.019679216533917247

4: 0.02256515576039871

5: 0.02540603527247574

10: 0.03869750099582716

20: 0.06016951688745736

30: 0.07597213357728104

40: 0.08783870545120151

-1: 22.58422122267688

-3: 37.77842304072701

-2: 1127.9896486631667

for key, value in sorted(temp_rss.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.01: 5.787885294027853

0.001: 5.9336671666847645

0.5: 5.951203188696909

0.0001: 5.978323815763974

1e-05: 6.052181151334658

1e-15: 6.090069263055022

1e-08: 6.090907261255897

1e-10: 6.09095577212052

1: 6.637661553114765

1.5: 7.34059814744305

2: 8.044716782843166

3: 9.446023936280277

4: 10.831274764991383

5: 12.194896930788355

10: 18.574800477997016

20: 28.881368105979536

30: 36.46662411709491

40: 42.16257861657673

-1: 10840.426186884908

-3: 18133.64305954895

-2: 541435.0313583203

Lasso:

Lasso adds penalty equivalent to the absolute value of the sum of coefficients. This penalty is added to the least square loss function and replaces the squared sum of coefficients from Ridge.

from sklearn.linear_model import Lasso

temp_rss = {}

temp_mse = {}

for i in alpha_ridge:

## Assigin each model.

lasso_reg = Lasso(alpha= i, normalize=True)

## fit the model.

lasso_reg.fit(X_train, y_train)

## Predicting the target value based on "Test_x"

y_pred = lasso_reg.predict(X_test)

mse = mean_squared_error(y_test, y_pred)

rss = sum((y_pred-y_test)**2)

temp_mse[i] = mse

temp_rss[i] = rss

for key, value in sorted(temp_mse.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.0001: 0.010061658258835855

1e-05: 0.011553103092552693

1e-08: 0.012464777509974378

1e-10: 0.012469892082710245

1e-15: 0.01246993993780167

0.001: 0.01834391027644981

0.01: 0.15998234085337285

0.5: 0.16529633945001213

1: 0.16529633945001213

1.5: 0.16529633945001213

2: 0.16529633945001213

3: 0.16529633945001213

4: 0.16529633945001213

5: 0.16529633945001213

10: 0.16529633945001213

20: 0.16529633945001213

30: 0.16529633945001213

40: 0.16529633945001213

-1: 14648689598.250006

-2: 58594759730.8125

-3: 131838210397.70003

for key, value in sorted(temp_rss.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.0001: 4.82959596424121

1e-05: 5.545489484425293

1e-08: 5.9830932047877035

1e-10: 5.985548199700918

1e-15: 5.9855711701448

0.001: 8.805076932695897

0.01: 76.79152360961895

0.5: 79.34224293600582

1: 79.34224293600582

1.5: 79.34224293600582

2: 79.34224293600582

3: 79.34224293600582

4: 79.34224293600582

5: 79.34224293600582

10: 79.34224293600582

20: 79.34224293600582

30: 79.34224293600582

40: 79.34224293600582

-1: 7031371007160.002

-2: 28125484670789.992

-3: 63282340990896.01

Elastic Net:

Elastic Net is the combination of both Ridge and Lasso. It adds both the sum of squared coefficients and the absolute sum of the coefficients with the ordinary least square function. Let’s look at the function.

from sklearn.linear_model import ElasticNet

temp_rss = {}

temp_mse = {}

for i in alpha_ridge:

## Assigin each model.

lasso_reg = ElasticNet(alpha= i, normalize=True)

## fit the model.

lasso_reg.fit(X_train, y_train)

## Predicting the target value based on "Test_x"

y_pred = lasso_reg.predict(X_test)

mse = mean_squared_error(y_test, y_pred)

rss = sum((y_pred-y_test)**2)

temp_mse[i] = mse

temp_rss[i] = rss

for key, value in sorted(temp_mse.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.0001: 0.010410247442255985

1e-05: 0.011786774263401294

1e-08: 0.012466548787037617

1e-10: 0.012469905615434403

1e-15: 0.012469939937937151

0.001: 0.014971538718578314

0.01: 0.10870291488354142

0.5: 0.16529633945001213

1: 0.16529633945001213

1.5: 0.16529633945001213

2: 0.16529633945001213

3: 0.16529633945001213

4: 0.16529633945001213

5: 0.16529633945001213

10: 0.16529633945001213

20: 0.16529633945001213

30: 0.16529633945001213

40: 0.16529633945001213

-3: 5.388825733568653

-2: 5.470945111059094

-1: 5.729175782943725

for key, value in sorted(temp_rss.items(), key=lambda item: item[1]):

print("%s: %s" % (key, value))

0.0001: 4.996918772282872

1e-05: 5.65765164643262

1e-08: 5.983943417778055

1e-10: 5.985554695408507

1e-15: 5.9855711702098295

0.001: 7.186338584917596

0.01: 52.17739914409985

0.5: 79.34224293600582

1: 79.34224293600582

1.5: 79.34224293600582

2: 79.34224293600582

3: 79.34224293600582

4: 79.34224293600582

5: 79.34224293600582

10: 79.34224293600582

20: 79.34224293600582

30: 79.34224293600582

40: 79.34224293600582

-3: 2586.6363521129515

-2: 2626.053653308364

-1: 2750.0043758129887

Fitting model (Advanced approach)

kfolds = KFold(n_splits=10, shuffle=True, random_state=42)

def rmsle(y, y_pred):

return np.sqrt(mean_squared_error(y, y_pred))

def cv_rmse(model, X=X):

rmse = np.sqrt(-cross_val_score(model, X, y, scoring="neg_mean_squared_error", cv=kfolds))

return (rmse)

alphas_alt = [14.5, 14.6, 14.7, 14.8, 14.9, 15, 15.1, 15.2, 15.3, 15.4, 15.5]

alphas2 = [5e-05, 0.0001, 0.0002, 0.0003, 0.0004, 0.0005, 0.0006, 0.0007, 0.0008]

e_alphas = [0.0001, 0.0002, 0.0003, 0.0004, 0.0005, 0.0006, 0.0007]

e_l1ratio = [0.8, 0.85, 0.9, 0.95, 0.99, 1]

ridge = make_pipeline(RobustScaler(), RidgeCV(alphas=alphas_alt, cv=kfolds))

lasso = make_pipeline(RobustScaler(), LassoCV(max_iter=1e7, alphas=alphas2, random_state=42, cv=kfolds))

elasticnet = make_pipeline(RobustScaler(), ElasticNetCV(max_iter=1e7, alphas=e_alphas, cv=kfolds, l1_ratio=e_l1ratio))

svr = make_pipeline(RobustScaler(), SVR(C= 20, epsilon= 0.008, gamma=0.0003,))

gbr = GradientBoostingRegressor(n_estimators=3000, learning_rate=0.05, max_depth=4, max_features='sqrt', min_samples_leaf=15, min_samples_split=10, loss='huber', random_state =42)

lightgbm = LGBMRegressor(objective='regression',

num_leaves=4,

learning_rate=0.01,

n_estimators=5000,

max_bin=200,

bagging_fraction=0.75,

bagging_freq=5,

bagging_seed=7,

feature_fraction=0.2,

feature_fraction_seed=7,

verbose=-1,

)

xgboost = XGBRegressor(learning_rate=0.01,n_estimators=3460,

max_depth=3, min_child_weight=0,

gamma=0, subsample=0.7,

colsample_bytree=0.7,

objective='reg:linear', nthread=-1,

scale_pos_weight=1, seed=27,

reg_alpha=0.00006)

stack_gen = StackingCVRegressor(regressors=(ridge, lasso, elasticnet, xgboost, lightgbm),

meta_regressor=xgboost,

use_features_in_secondary=True)

# score = cv_rmse(stack_gen)

score = cv_rmse(ridge)

print("Ridge: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

score = cv_rmse(lasso)

print("LASSO: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

score = cv_rmse(elasticnet)

print("elastic net: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

score = cv_rmse(svr)

print("SVR: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

score = cv_rmse(lightgbm)

print("lightgbm: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

# score = cv_rmse(gbr)

# print("gbr: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

score = cv_rmse(xgboost)

print("xgboost: {:.4f} ({:.4f})\n".format(score.mean(), score.std()), datetime.now(), )

Ridge: 0.1011 (0.0141)

2020-01-22 15:12:38.941969

LASSO: 0.0997 (0.0142)

2020-01-22 15:12:45.519931

elastic net: 0.0998 (0.0143)

2020-01-22 15:13:12.882048

SVR: 0.1020 (0.0146)

2020-01-22 15:13:26.262319

lightgbm: 0.1054 (0.0154)

2020-01-22 15:13:44.348901

[15:13:44] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:13:58] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:14:12] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:14:28] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:14:42] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:14:55] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:15:09] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:15:25] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:15:39] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:15:53] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

xgboost: 0.1061 (0.0147)

2020-01-22 15:16:07.581332

print('START Fit')

print('stack_gen')

stack_gen_model = stack_gen.fit(np.array(X), np.array(y))

print('elasticnet')

elastic_model_full_data = elasticnet.fit(X, y)

print('Lasso')

lasso_model_full_data = lasso.fit(X, y)

print('Ridge')

ridge_model_full_data = ridge.fit(X, y)

print('Svr')

svr_model_full_data = svr.fit(X, y)

# print('GradientBoosting')

# gbr_model_full_data = gbr.fit(X, y)

print('xgboost')

xgb_model_full_data = xgboost.fit(X, y)

print('lightgbm')

lgb_model_full_data = lightgbm.fit(X, y)

START Fit

stack_gen

[15:17:42] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:17:54] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:18:07] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:18:21] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:18:34] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:18:54] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

[15:19:15] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

elasticnet

Lasso

Ridge

Svr

xgboost

[15:19:40] WARNING: /workspace/src/objective/regression_obj.cu:152: reg:linear is now deprecated in favor of reg:squarederror.

lightgbm

Blending Models

1.0 * elastic_model_full_data.predict(X)

array([12.2252765 , 12.19482971, 12.28743582, ..., 12.45057568,

11.846052 , 11.9162269 ])

def blend_models_predict(X):

return ((0.1 * elastic_model_full_data.predict(X)) + \

(0.05 * lasso_model_full_data.predict(X)) + \

(0.2 * ridge_model_full_data.predict(X)) + \

(0.1 * svr_model_full_data.predict(X)) + \

# (0.1 * gbr_model_full_data.predict(X)) + \

(0.15 * xgb_model_full_data.predict(X)) + \

(0.1 * lgb_model_full_data.predict(X)) + \

(0.3 * stack_gen_model.predict(np.array(X))))

print('RMSLE score on train data:')

print(rmsle(y, blend_models_predict(X)))

RMSLE score on train data:

0.06279142797823006

submission = pd.read_csv("../input/house-prices-advanced-regression-techniques/sample_submission.csv")

submission.iloc[:,1] = np.floor(np.expm1(blend_models_predict(X_sub)))

Predict submission

Submission

q1 = submission['SalePrice'].quantile(0.005)

q2 = submission['SalePrice'].quantile(0.995)

submission['SalePrice'] = submission['SalePrice'].apply(lambda x: x if x > q1 else x*0.77)

submission['SalePrice'] = submission['SalePrice'].apply(lambda x: x if x < q2 else x*1.1)

submission.to_csv("submission.csv", index=False)

Reference

Notebooks in kaggle:

House Prices: 1st Approach to Data Science Process

Stack&Blend LRs XGB LGB {House Prices K} v17